The recent surge in government bond yields has forced business leaders and investors around the world to confront a critical question: Should corporations lock in debt at current interest rates before they rise further? At the same time, higher capital costs and persistent market volatility are compelling investors to reassess their portfolios.

The question has become increasingly urgent as the yield on ten-year US Treasuries has climbed 50 basis points to 4.5% in less than a month. The yield on 30-year Treasuries is approaching 5% after rising 30 basis points in May alone.

Beyond short-term market swings, at least five structural shifts could reshape the global economic landscape, with the potential to upend corporate strategies, erode investment returns, and further undermine growth prospects.

First, there is the United States’ deteriorating fiscal position. The Congressional Budget Office’s latest forecast assumes a ten-year Treasury yield of 4.1% in 2025, falling to 3.8% by 2035. But given that the ten-year yield is already hovering around 4.5% and interest rates are expected to stay elevated, the federal deficit could expand far more quickly than previously anticipated.

America’s fiscal trajectory is already unsustainable, with the CBO projecting that the federal budget deficit will increase from 6.2% of GDP in 2025 to 7.3% by 2055. Even more alarming, the debt-to-GDP ratio – currently 124.3% of GDP – could reach 156% by 2055 if current trends persist.

The second source of uncertainty involves credit default swaps (CDS), which helped fuel the 2007-08 global financial crisis. Since Moody’s downgraded America’s sovereign credit rating from triple-A to Aa1 in May, the cost of insuring against a US default has risen sharply, as markets increasingly treat US government debt as a higher-risk asset.

In fact, US CDS spreads now exceed those of countries with a similar credit rating, such as the United Kingdom, and are trading at levels comparable to those of Greece and Italy, both of which are rated BBB. Similarly, insuring US government debt now costs more than insuring Chinese government bonds, despite China’s lower A1 rating.

A third issue is the opacity of private credit markets, which represents a long-term structural vulnerability. BlackRock predicts that private credit assets under management will more than double to $4.5 trillion by 2030. As more capital flows into private markets – both equity and debt – pricing becomes less transparent, making it harder for investors to value assets.

The continued expansion of opaque private markets also increases the risk of leverage building up unnoticed. Much of this debt lies beyond the reach of regulatory oversight, leaving analysts and policymakers without the data needed to assess or model the true extent of systemic risk.

In an environment marked by growing uncertainty, they must be prepared to adjust their portfolios and capital-allocation strategies to account for a wider range of risks and potential outcomes.

Unregulated credit markets may be especially vulnerable to cascading failures, while persistently elevated interest rates heighten the risk of default. If left unaddressed, these vulnerabilities could result in widespread financial distress and job losses, ultimately triggering an economic downturn.

Fourth, the relationship between the US dollar and interest rates appears to be changing. Historically, rising bond yields have supported a stronger dollar, while falling yields tended to weaken it.

Since late March, however, bond yields have climbed even as the dollar has declined by 6% against the euro. This divergence suggests that global markets are repricing the premium on holding dollars and are now demanding higher returns.

US stocks have also been volatile, suggesting that the repricing of risk premiums on dollar-denominated assets extends to equity markets. Rising yields reduce the value of existing bonds, signaling that Treasuries are no longer viewed as a reliable hedge against stock-market turbulence.

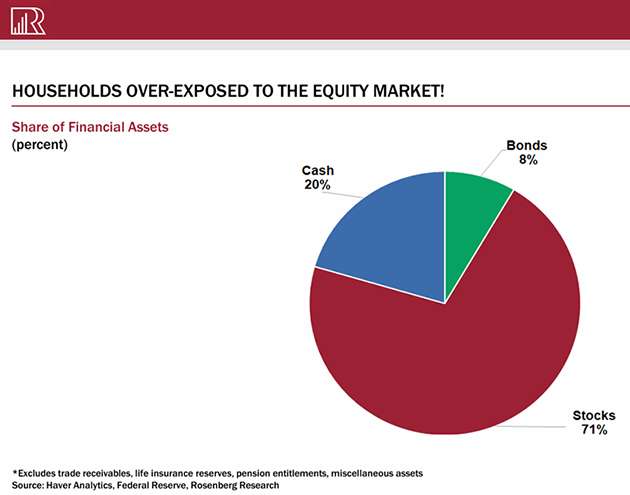

Lastly, many Americans remain heavily exposed to equities. According to one estimate, stocks account for more than 70% of US households’ financial assets. This makes the recent surge in bond yields and the rise in economic uncertainty particularly concerning, as both developments point to fundamental shifts in market dynamics.

The business leaders and investors most likely to succeed in this rapidly shifting landscape will be those who grasp the far-reaching implications of economic and geopolitical trends.

In an environment marked by growing uncertainty, they must be prepared to adjust their portfolios and capital-allocation strategies to account for a wider range of risks and potential outcomes.

(Dambisa Moyo is an international economist)

Copyright: Project Syndicate

{kind=link}

Comment