Loading...

0%

Under the leadership of President Mohamed Muizzu, the islands of the Maldives find themselves ensnared in an economic quagmire, with their financial sovereignty hanging precariously in the balance.

The nation’s mounting debt owed to China has reached alarming proportions, casting a dark shadow over its future and raising grave concerns about the long-term implications of this precarious partnership.

The raw numbers paint a sobering picture of the Maldives’ deepening debt crisis.

According to a World Bank report, the island nation’s debt to China has skyrocketed to a staggering $1.37 billion, accounting for a whopping 20% of its total public debt.

This debt trap, once warned about by former President Mohamed Nasheed, has now become a grim reality, with the Maldives’ economic health held hostage by its largest bilateral creditor.

The consequences of this debt crisis are already being felt, with interest payments on external loans surging by 15% from January to August 2023, reaching an eye-watering $162.3 million.

The World Bank’s report highlights a worrying “build-up of sovereign exposure” and a “lack of domestic investment opportunities” during the pandemic, painting a bleak picture of the economic challenges facing the Maldives.

The economic woes plaguing the Maldives are further compounded by the nation’s recurring expenditure, which continues to rise unchecked, while capital expenditure is increasingly funded through external debt or deficit-financing.

President Muizzu’s recent desperate pleas to China for debt restructuring only underscore the gravity of the situation.

His direct appeal to Chinese President Xi Jinping, seeking a grace period on loan repayments over the next five years, is a clear admission of the Maldives’ inability to service its debt obligations.

This move places the nation in a perilous position, with the International Monetary Fund (IMF) classifying its risk of external debt distress as ‘high.’

The global context further underscores the perils of the Maldives’ entanglement with China.

The cautionary tales of Sri Lanka and Pakistan, both grappling with economic crises after extensive Chinese investments, should serve as a wake-up call for the Muizzu administration.

The Maldives must navigate this economic minefield with utmost caution, lest it sacrifices its sovereignty at the altar of short-term debt relief.

Alarmingly, President Muizzu’s economic policies have seen a troubling shift away from the Maldives’ traditional partners.

While India has been a reliable ally, providing cost-effective healthcare solutions and developmental aid, Muizzu’s overtures towards Western countries like the US and Europe risk disrupting these established networks.

The unique geographical challenges of the Maldives make India’s regional proximity and longstanding partnership a far more economically viable choice.

The government’s decision to bolster spending amid proposed reforms reeks of fiscal imprudence, suggesting a lack of strategic economic management and a disturbing disregard for the nation’s long-term financial health.

Yet, Muizzu seems intent on charting a new course, one that could lead to increased costs for medical services and potential losses in developmental assistance.

Furthermore, the President’s call for the removal of ‘foreign soldiers’ from Maldivian soil, a thinly veiled jab at India’s security presence, has created a diplomatic rift with a vital partner.

Despite Prime Minister Narendra Modi’s efforts to maintain strong bilateral relations, Muizzu’s insistence on addressing this issue has cast a pall of uncertainty over the future of Indo-Maldivian ties.

The economic woes plaguing the Maldives are further compounded by the nation’s recurring expenditure, which continues to rise unchecked, while capital expenditure is increasingly funded through external debt or deficit-financing.

This reckless financial management raises serious questions about the sustainability of such practices and the potential long-term consequences for the nation’s economic stability.

President Muizzu’s tenure has been a stark display of poor economic stewardship, as the Maldives grapples with a litany of challenges.

The much-touted economic expansion in Q1 2023 and the increase in tourist arrivals have been overshadowed by a concerning 3.5 percent inflation rate in H1 2023 and a doubling of the current account deficit.

The nation’s leadership seems intent on charting a perilous course, one that mortgages the country’s economic future to China while alienating long-standing partners like India.

The government’s decision to bolster spending amid proposed reforms reeks of fiscal imprudence, suggesting a lack of strategic economic management and a disturbing disregard for the nation’s long-term financial health.

The Maldives’ descent into economic turmoil has been further exacerbated by President Muizzu’s recent overtures to China for additional financial assistance.

Shockingly, the Maldivian government has requested a staggering $550 million from China to meet its budgetary requirements for 2024.

This includes a $200 million grant-aid and a $350 million loan at concessional rates, further deepening the nation’s dependence on Chinese largesse.

While Muizzu triumphantly announced that his visit to China was “fruitful,” with promises of a $130 million grant-aid and a potential restructuring of existing loans, the reality is far less rosy.

Aside from a paltry $10 million received during the visit, the Maldives has yet to see any tangible financial support from China, leaving the nation’s economic future hanging in the balance.

The hard facts paint a grim picture: as of September 2023, the Maldives’ total public debt, including borrowings and sovereign guarantees, stood at a staggering 110.9% of GDP. Foreign debt as a percentage of GDP stood at 47.5%, with the nation owing a whopping $600 million to China alone.

The bulk of this debt is in the form of sovereign guarantees for loans taken through various government companies, exposing the Maldives to significant financial risk.

Unless a radical change in approach is undertaken, the Maldives is headed down a path of no return, with its once-vibrant economy shackled by the weight of Chinese debt, and its sovereignty reduced to a mere illusion.

President Muizzu’s diplomatic maneuvers have created a cloud of uncertainty around the future trajectory of the Maldives’ bilateral relations.

The nation’s leadership seems intent on charting a perilous course, one that mortgages the country’s economic future to China while alienating long-standing partners like India.

As the Maldives teeters on the brink of an economic abyss, the decisions made by President Muizzu and his administration will have far-reaching consequences.

The choices made today will shape the economic future of the nation and its people, determining whether the Maldives emerges from this crisis with its sovereignty intact or becomes another cautionary tale of a country ensnared in China’s debt trap diplomacy.

President Muizzu’s recent re-election victory in the 2024 polls paints a darker picture for the Maldives’ economic future.

With his administration’s policies firmly entrenching the nation deeper into China’s debt trap, the prospects for course correction seem increasingly bleak.

Muizzu’s re-election is a damning indictment of the Maldivian people’s economic illiteracy, paving the way for the country’s complete economic subjugation to Beijing’s neo-colonial ambitions.

Unless a radical change in approach is undertaken, the Maldives is headed down a path of no return, with its once-vibrant economy shackled by the weight of Chinese debt, and its sovereignty reduced to a mere illusion.

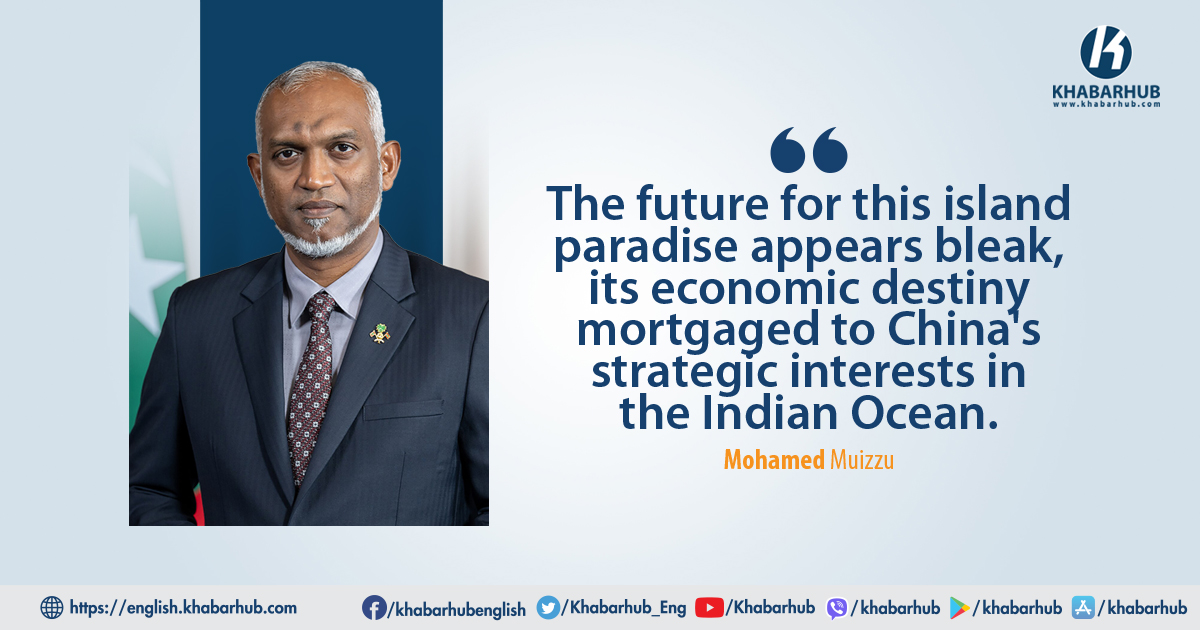

The future for this island paradise appears bleak, its economic destiny mortgaged to China’s strategic interests in the Indian Ocean.